(This essay was published in Hong Kong Economic Journal on 17 May 2017.)

We often hear laments and protests that ‘housing is for living, not for speculation’ whenever housing demand increases faster than supply can catch up and speculation becomes rife in the market place. Faced with populist political pressure, most governments cannot wait for housing supply to increase. They have to tackle the problem of housing shortage immediately.

Governments looking for quick fixes often deal with the symptom of housing price increases by suppressing demand and limiting speculation. Speculators are targeted as the public enemy for disrupting market order. They are trashed for acquiring housing units to turn a profit rather than to live in.

Speculators are detested because most people simply reason that every housing unit they purchase and hoard removes its immediate availability to those who are in need of a place to live. They point to landlords keeping units vacant in order to sell them later rather than renting them out immediately. But such populist narratives fail to recognize that speculation is the outcome of housing shortages and not its cause.

Sometimes governments are worried about the dangers that runaway property prices will pose to banking and financial stability so they try to tighten credit conditions by lowering the loan-to-value ratio. They require purchasers to put up a higher share of the property value as down payment towards a mortgage loan.

Curbing Speculation

Government interventions into the Hong Kong housing market started in 1991 after several years of rising property prices. In a bid to stop speculative activities, the loan-to-value ratio for residential housing was lowered from 90% to 70%, the number of units reserved by developers for internal sales was limited to 50% of total flats available, and confirmor transactions of pre-sold units (i.e., forward delivery) were subjected to stamp duty.

But market confidence was unabated. So, in a further bid to limit speculative activities, in 1994 the government limited the pre-sale of residential units under construction to at most 9 months before completion, and buyers had to pay a 10% deposit instead of 5% on residential property transactions. These anti-speculation measures were removed in stages as residential property prices slumped after the 1997 Asian financial crisis.

Housing price began to recover after 2003 and speculative activities again started to emerge. In 2009, confirmor transactions for units under construction were banned, the loan-to-value ratio was lowered to 60% for properties in excess of $12 million, and stamp duties were raised again. In 2011, the loan-to-value ratio was lowered to 50%.

After 2012, higher stamp duties were imposed on foreign purchases and second-time buyers to limit investment demand in the housing market, and a capital gain levy was imposed on short-term transaction profits.

For all practical purposes, speculation – defined as short-term profiteering activities to purchase and hoard real estate – has been eliminated from the market. But the draconian punitive measures used to dampen housing demand did not prevent housing prices from soaring again in late 2016.

Why have property prices continue to rise even when the government appears to be totally committed to supplying more housing units, rooting out all speculation and limiting certain forms of investment activities?

Underlying Demand and Chasing After Yields

Two factors are operating at the same time. First, the public recognizes that the scale of the supply shortage is sufficiently large that it cannot be eliminated quickly through more construction unless housing prices correct downwards for some other external reason. Second, at present the market is still chasing after yields as a result of a protracted, low interest rate environment.

The first factor has many underlying social and economic causes. Difficulties in assembling and converting agricultural land and reclaiming land slow down housing supply. The shortage of construction workers also slows down housing supply. The continued reliance on the public rental housing program to meet the rising demand for affordable housing generates perverse effects that create yet more demand growth for two reasons.

Firstly, adult children in public rental housing have to deregister from their parents’ household, pushing them onto the waiting list for new public rental housing. So while private sector units can be sub-divided, public rental units cannot. Secondly, public rental housing households that are divorced can apply for a second unit if one party becomes remarried and many find new spouses across the border.

The second factor is the unconventional monetary policy practiced in the US, Europe and Japan since the 2008 financial crisis. Quantitative easing created an abundance of cheap credit and pushed investors to chase after yields. The low interest rates induce investors to seek alternative ways to generate returns. By chasing after yields, investors end up assuming higher risk that might be mispriced. It also provides an artificial stimulus to interest-sensitive sectors, such as housing.

Since the housing sector is typically a low-productivity sector, it results in an overall reduction in the productivity of the economy. As a consequence, there is a co-existence of slow economic growth and high property prices.

The world economy is beginning to show some encouraging signs of recovery after almost eight years of lethargic growth. This would conventionally mean interest rates should be increasing, so why are investors still chasing after yield at a time when real estate prices are already so high?

Chasing After Yields

Under conventional circumstances both fiscal and monetary policies will be used to stimulate economic recovery after a financial crisis. But debt levels in almost all the advanced economies are at record high levels and they are mostly concentrated in the public sector. The sector’s debt-servicing requirements would automatically increase if there were a normalization of interest rates (i.e., raising interest rates) at this time. Fiscal spending in other areas could immediately come under pressure. And this could ignite fears that the economic recovery would stall.

So, adopting a compensatory fiscal stimulus to offset the effects of monetary tightening appears to be difficult given the already high levels of public debt and the potential risk of damaging the still fragile credibility of the government. The economic policy environment in advanced economies is now almost entirely dependent on a single policy instrument – monetary policy. The central bank is the only policy game in town and this is woefully insufficient.

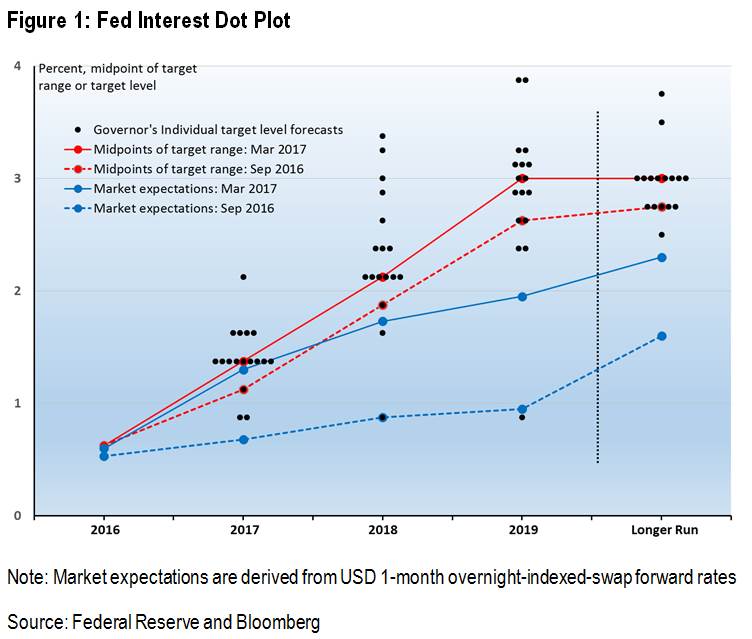

The market knows this and it is not convinced that central banks will follow through on raising interest rates despite what their stated intentions. The US Federal Reserve Open Market Committee (FOMC) under Benjamin Bernanke decided to publish the individual target forecasts of each governor showing where they thought the interest rate would be in the future. The dot plots of these individual forecasts, which are published every quarter, and the midpoints of the target range after the September 2016 and March 2017 FOMC meetings are given in the Figure. Typically the range on the individual forecasts varies by more than one percentage point.

The significant fact to note is that market expectations of where the interest rate will be are consistently below the target forecasts of the Fed governors. Market expectations are derived from USD 1-month overnight-indexed-swap forward rates.

As recently as March 2017, the difference was over 30 basis points for 2018 and 100 basis points for 2019.

One can speculate endlessly about why market expectations are lower than Fed targets, and are even lower in 2019 than in 2018. I believe the key point is that the market does not believe the Fed follows any rules now in determining its interest rate policy, but will continue to exercise judgment and discretion as it has been doing in the past few years. This encourages the market to bet on what the Fed will do next and some in the market will continue to chase after yields and seek alternative ways to generate returns. It is likely that these investors will end up assuming higher risk, which might be mispriced.

Will this justify introducing more restrictions to limit market transactions and clamp down on speculation? In the Hong Kong context, will further intervention in the private property market and the market for mortgage and development loans serve the public interest? Whose interest will it serve?

Curbing Short-Term Speculation

Whenever there are imbalances in the market, there is no simple way of limiting speculation without harming the market adjustment process. Limiting speculation and even trying to drive it out often worsens the shortage and can even destabilize the market when demand and supply conditions reverse.

Common measures to limit speculation include capital gains taxes on short-term transactions, transactions levies, levies on transactions using company structures, levies on overseas buyers and non-first time buyers, levies on vacancies, and regulating loan-to-value ratios.

These measures do not reduce or eliminate demand. They merely drive a wedge between the prices buyers pay and the amount that suppliers receive. As a result, they reduce the transactions volume in the short-run and drive down the prices suppliers would have otherwise charged. Over time, their effect on dampening demand disappears, although short-term speculative activities will naturally be eliminated as a consequence.

However, the elimination of short-term speculators in the market is not neutral in the long run. Four obvious effects are discernible. First, it reduces liquidity. Markets become more volatile because transactions become thinner.

Second, the thinning of transactions affects the secondary market more than the primary market because developers are often able to provide financing arrangements for buyers, which are unavailable from individual vendors in the secondary market. This has the result of driving up the price of units in the primary market relative to the secondary market.

Third, the thinning of markets and the migration of transactions to the primary market creates a noisier price signal of the underlying supply and demand conditions in the market. In particular, the thinning of the large secondary market has the unfortunate effect of slowing the release of these units onto the market. The overall effect is to reduce the supply of secondary units to the market and further exacerbate price increases.

Fourth, regulating the loan-to-value ratio makes it more difficult for all buyers to enter the market because of higher down payments. The effect is most unfortunate for credit-worthy buyers who have not saved up enough to enter the market. Their purchases are delayed and they may have to buy at a higher price and assume a higher level of risk. In general, market opportunities are shifted from less capitalized buyers to more capitalized ones, equality of opportunity worsens and economic inequality increases.

Regulating the loan-to-value ratio is justified if the public is heavily leveraged. This protects financial stability by limiting the exposure of banks and other financial intermediaries to systemic risks and the mispricing of risk. But it has a very marginal effect on protecting financial stability if leverage is not high in the market place. Curbing speculation and market regulation is therefore not always an improvement and will depend on circumstances. In a situation of ‘second-best’, there are often no ‘first-best’ choices.

Hong Kong investors in the property market should be worried that market expectations of future interest rate targets are not presently aligned with Fed targets. There is greater risk that markets may be surprised by Fed decisions to normalize, so that they wake up one morning to discover their bets had been wrong. When this happens, it is important for markets to be able to adjust quickly to interest rate normalization—excessive regulations and restrictions are of no help.